Accounting is the art of recording, classifying and summarizing, in a significant manner, and in terms of money, transactions and events which are, in part at least of a financial character, and interpreting the results thereof.

Accounting is the science of

recording and classifying business transactions and events, primarily of a

financial character, and the art of making significant summaries,

analysis and interpretations of these transactions and events and communicating

the result to persons who must make decisions or form judgments. - Herold Bierman and Allan R. Drebin

Accounting may be defined as the

process of collecting, recording, summarizing and communicating financial

information.

Accounting refers to the

system involved in making a financial record of business transactions and in

the preparation of statements concerning the assets, liabilities, capital and

operating results of the business.

Accounting is nothing but a

means of communicating the results of business operations to varies parties

interested in or connected with the business, viz., the owner, creditors,

investors, government, financial institutions and other agencies. Accounting is,

therefore, rightly called as the language of business.

The basis purpose of a

language is to serve as a means of communication. Accounting also serves this

purpose. Accounting is not only associated with business but also with every

body who is interested in keeping an account for the money received and money

spent.

basis purpose of a language is to serve as a means of communication. Accounting also serves this purpose. Accounting is not only associated with business but also with every body who is interested in keeping an account for the money received and money spent.

Nature of Accounting:- The

analysis of the above definitions brings out the following as attributes of

accounting:

- It is the art of recording and

classifying business transactions and events.

- The events and transactions of

a financial nature must be recorded in monetary terms, while the events

and transactions of a non-financial nature cannot be recorded.

- The record should reflect the

importance of the transactions so recorded both individually and

collectively, which includes summarization, thereby making it amenable to

analysis.

- The users of the financial

statements should be able to obtain the message encompassed in such

financial statements, and it is the knowledge of accounting, which enables

the user to understand the contents of the financial statements.

Objectives

of Accounting

·

As

an information system, the basic objective of accounting is to provide useful

information to the interested group of users, both external and internal. The

necessary information, particularly in case of external users, is provided in

the form of financial statements, viz., profit and loss account and balance

sheet.

·

Besides

these, the management is provided with additional information from time to time

from the accounting records of business.

The primary objectives of accounting include the following:

- Maintaining

Accounting Records

- Ascertainment

of Profit or Loss

- Ascertainment

of Financial Position

- Communication

of Information

Scope of Accounting:- Accounting plays a

key role in serving a systematic and up-to-date record of varied and numerous

business transactions. Its target is to analyse the financial transactions as

they take place, to record them in orderly fashion, to group and arrange the information

in terms of useful and understandable financial report (Balance Sheet, Income

Statement) and to assist in the process of interpretation.

Accounting is a service activity. Its function is to

provide quantitative information, primarily financial in nature, about economic

entities that is useful in making economic decisions, in making reasoned

choices among alternative course of action.

Accounting is thus not

an end itself but a means to an end. It is mainly a service function. In broad

perspective an accounting system should concern itself with the following

information:

- Analysis of past financial data

to find out the reasons for bad condition of the concern and corrective

measures for improvement of the business.

- Accounting is an art, on the

other hand, it is the application of knowledge comprising of some accepted

theories, rules, concepts and conventions. It helps us to achieve our

goals and tells us the manner in which we may attain our objectives in the

best possible way. The more we practice an art the more expert we become

in it.

- Accounting is a science because

recording, classifying and summarising of business transactions is done on

the basis of certain principles of double entry system which are

universally applicable.

- Accounting seems to be very

important in financial forecasting and financial forecasting helps in

estimating the profitable projects and out of these profitable projects

accountant chooses the one which is more profitable for the concern.

- For decision-making accounting

is useful. Accounting helps the accountants to take decision about capital

structures, cost of capital, an ideal capital gearing ratio, capital

budgeting, working capital, cash, budget, cost control, inventory

management etc.

- Accounting is a technique which

compares the cost of various departments and thus find out which

department is efficient than the other.

- As is common with physicians,

engineers, lawyers, and architects, accountants (including CPAs) commonly

are engaged in professional practice or are employed by business,

government entities, non-profit organisations and so on.

Accounting can be

classified into the following categories:

Ø Financial accounting

Ø Management accounting (including Cost

accounting

Ø Auditing

Ø Others like Price level changes accounting,

Social cost accounting, Social auditing, Human resource accounting, Forensic

accounting, Creative accounting, Value added accounting etc.

Book keeping

Recording of financial transactions in a proper manner related to the business operation of an entity is known as book- keeping. Book -keeping is the permanent recording of financial transactions in a proper manner in the books of accounts of an entity so that their financial effect on the business of entity can be seen. There is a difference between the two terms bookkeeping and accounting.

Book-keeping and accounting are different from each other. Bookkeeping is an important part of accounting. Accounting is broader than book-keeping. Accounting includes a design of accounting systems which book-keepers use for the preparation of financial statements, audits, cost studies, income-tax statements etc.

There is a difference between the two terms bookkeeping and accounting, let us understand what is bookkeeping and accounting, their processes and difference between the two. While doing Bookkeeping, we need to follow the basic accounting concepts and accounting conventions.

Bookkeeping is clerical in nature. Book-keeping is usually done by junior employees of the entity. Most of the entities nowadays use computers for bookkeeping rather than recording them manually. Accounting of an entity depends on its book-keeping system.

Book-keeping is the basis for accounting. It is because it is responsible for the proper recording of financial transactions. Whereas, Accounting involves classification, summarizing and reporting of financial transactions. It involves the preparation of source documents for all the financial transactions of the entity.

.png)

.png)

.png)

.jpeg)

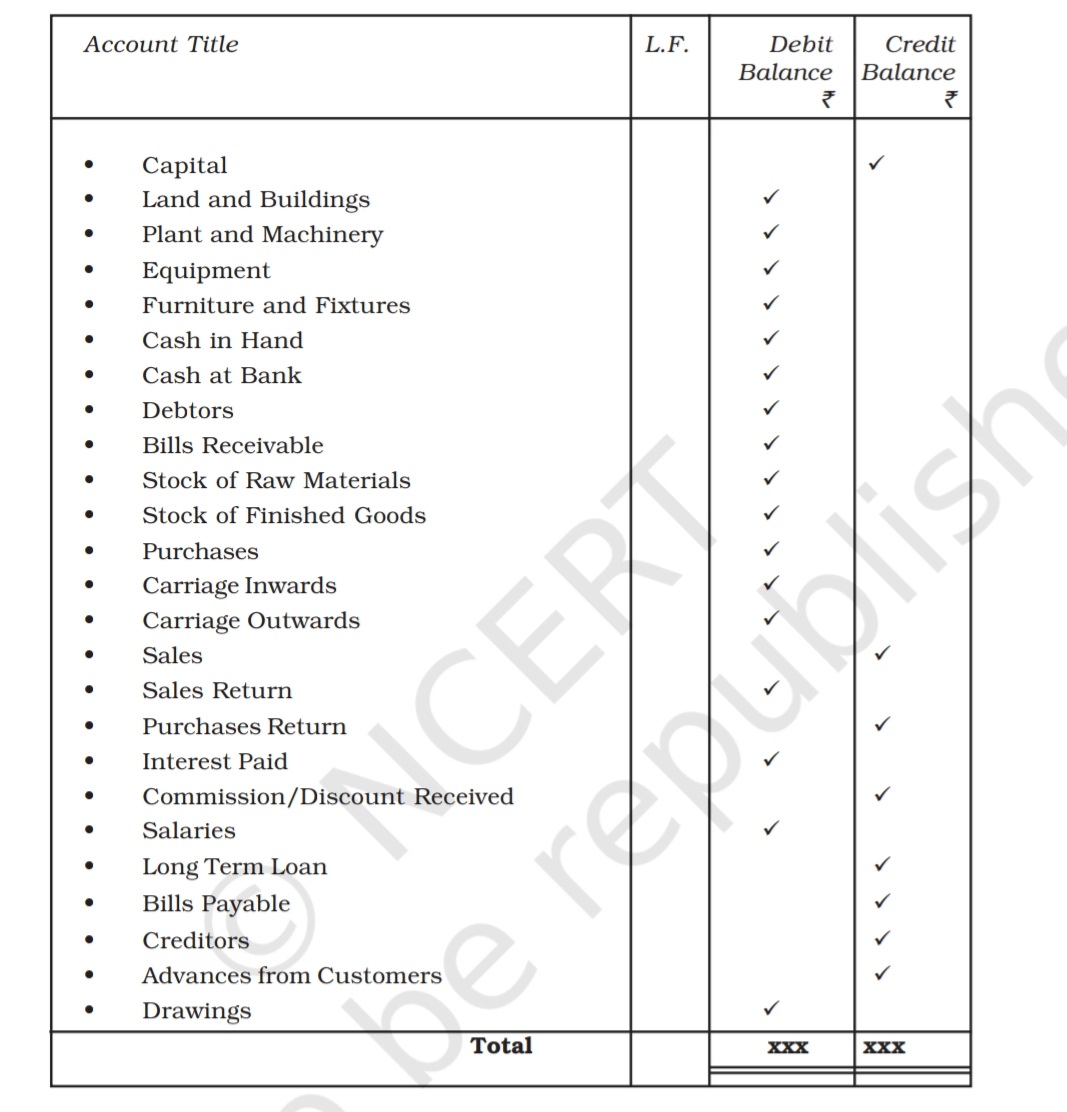

LEDGER

All

the accounts identified on the basis of transactions recorded in different journals/books

such as Cash Book, Purchase Book, Sales Book etc. will be opened and maintained

in a separate book called Ledger. So a ledger is a book of account; in which

all types of accounts relating to assets, liabilities, capital, expenses and

revenues are maintained. It is a complete set of accounts of a business

enterprise.

Thus, from the various journals/Books of a business enterprise, all transactions recorded throughout the accounting year are placed in relevant accounts in the ledger through the process of posting of transactions in the ledger. Thus, posting is the process of transfer of entries from Journal/Special Journal Books to ledger.

Features of ledger:-

- Ledger

is an account book that contains various accounts to which various business

transactions of a business enterprise are posted.

- It

is a book of final entry because the transactions that are first entered in the

journal or special purpose Books are finally posted in the ledger. It is also

called the Principal Book of Accounts.

- In

the ledger all types of accounts relating to assets, liabilities, capital, revenue

and expenses are maintained.

- It

is a permanent record of business transactions classified into relevant accounts.

- It

is the ‘reference book of accounting system and is used to classify and

summarise transactions to facilitate the preparation of financial statements.

Importance of Ledger:- Ledger is an important book of Account. It contains all the accounts in which all the business transactions of a business enterprise are classified. At the end of the accounting period, each account will contain the entire information of all the transactions relating to it. Following are the advantages of ledger.

Knowledge of Business results:- Ledger provides detailed information about revenues and expenses at one place. While finding out business results the revenue and expenses are matched with each other.

· Knowledge of book value of assets:- Ledger records

every asset separately. Hence, you can get the information about the Book value

of any asset whenever you need.

· Useful for management:- The information

given in different ledger accounts will help the management in preparing

budgets. It also helps the management in keeping the check on the performance

of business it is managing.

· Knowledge of Financial Position:- Ledger provides

information about assets and liabilities of the business. From this we can

judge the financial position and health of the business.

· Instant Information:- The business

always need to know what it owes to others and what the others owe to it. The

ledger accounts provide this information at a glance through the account

receivables and payables.

What Is a

Budget?

A budget is an

estimation of revenue and expenses over a specified future

period of time and is usually compiled and re-evaluated on a periodic basis. Budgets can

be made for a person, a group of people, a business, a government, or just

about anything else that makes and spends money.

To manage your

monthly expenses, prepare for life's unpredictable events, and be able to

afford big-ticket items without going into debt, budgeting is important.

Keeping track of how much you earn and spend doesn't have to be drudgery,

doesn't require you to be good at math, and doesn't mean you can't buy the

things you want. It just means that you'll know where your money goes, you'll

have greater control over your finances.

Understanding Budgeting:- A budget is a microeconomic

concept that shows the trade-off made when one good is exchanged for another.

In terms of the bottom line—or the end result of this trade-off—a surplus

budget means profits are anticipated, a balanced budget means

revenues are expected to equal expenses, and a deficit budget means

expenses will exceed revenues.

What are Financial

Statements :- Financial statements are

a collection of summary-level reports about an organization's financial

results, financial position, and cash flows. They include the income statement,

balance sheet, and statement of cash flows.

Advantages of Financial

Statements:- Financial Statements are

useful for the following reasons:

Ø

To

determine the ability of a business to generate cash, and the sources and uses

of that cash.

Ø

To

determine whether a business has the capability to pay back its debts.

Ø

To

track financial results on a trend line to spot any looming profitability

issues.

Ø

To

derive financial ratios from the statements that can indicate the condition of

the business.

Ø

To

investigate the details of certain business transactions, as outlined in the

disclosures that accompany the statements.

Ø

To

use as the basis for an annual report, which is distributed to a company’s

investors and the investment community.

Disadvantages of

Financial Statements:-

There are few downsides

to issuing financial statements. A possible concern is that they can be

fraudulently manipulated, leading investors to believe that the issuing entity

has produced better results than was really the case. Such manipulation can

also lead a lender to issue debt to a business that cannot realistically repay

it.

Balance Sheet:-

The term balance sheet refers to a financial

statement that reports a company's assets, liabilities, and shareholder equity

at a specific point in time. Balance sheets provide the basis for computing

rates of return for investors and evaluating a company's capital structure. In short, the balance sheet is a financial statement that provides a snapshot of what a

company owns and owes, as well as the amount invested by shareholders. Balance

sheets can be used with other important financial statements to conduct

fundamental analysis or calculating financial ratios.

The balance sheet adheres to the

following accounting equation, with assets on one side, and liabilities plus

shareholder equity on the other, balance out:

Assets = Liabilities + Shareholders' Equity

This formula is intuitive. That's

because a company has to pay for all the things it owns (assets) by either

borrowing money (taking on liabilities) or taking it from investors (issuing

shareholder equity)

Components of a Balance Sheet:-

Assets:- Accounts within this segment are listed from top to

bottom in order of their liquidity. This is the ease with which

they can be converted into cash. They are divided into current assets, which

can be converted to cash in one year or less; and non-current or long-term

assets, which cannot.

Here is the general

order of accounts within current assets:

- Cash and

cash equivalents are the most liquid assets and can include Treasury

bills and short-term certificates of deposit, as well as hard currency.

- Marketable

securities are equity and debt securities for which there is a liquid

market.

- Accounts

receivable (AR) refer to money that customers owe the company. This

may include an allowance for doubtful accounts as some customers may not

pay what they owe.

- Inventory

refers to any goods available for sale, valued at the lower of the cost or

market price.

- Prepaid expenses represent the value that has already been paid for, such as insurance, advertising contracts, or rent.

Long-term assets

include the following:

- Long-term

investments are securities that will not or cannot be liquidated in the

next year.

- Fixed

assets include land, machinery, equipment, buildings, and other

durable, generally capital-intensive assets.

- Intangible

assets include non-physical (but still valuable) assets such as

intellectual property and goodwill. These assets are generally only listed

on the balance sheet if they are acquired, rather than developed in-house.

Their value may thus be wildly understated (by not including a globally

recognized logo, for example) or just as wildly overstated.

Liabilities:- A liability is any money that a

company owes to outside parties, from bills it has to pay to suppliers to

interest on bonds issued to creditors to

rent, utilities and salaries. Current liabilities are due within one year and

are listed in order of their due date. Long-term liabilities, on the other

hand, are due at any point after one year.

Current liabilities accounts

might include:

- current

portion of long-term debt

- bank

indebtedness

- interest

payable

- wages

payable

- customer

prepayments

- dividends

payable and others

- earned

and unearned premiums

- accounts

payable

Long-term liabilities can

include:

- Long-term

debt includes any interest and principal on bonds issued

- Pension

fund liability refers to the money a company is required to pay into its

employees' retirement accounts

- Deferred

tax liability is the amount of taxes that accrued but will not be

paid for another year. Besides timing, this figure reconciles differences

between requirements for financial reporting and the way tax is

assessed, such as depreciation calculations.

Why Is a Balance Sheet

Important?

The balance sheet is an essential tool used by executives, investors, analysts, and regulators to understand the current financial health of a business. It is generally used alongside the two other types of financial statements: the income statement and the cash flow statement.

Balance sheets allow

the user to get an at-a-glance view of the assets and liabilities of the

company. The balance sheet can help users answer questions such as whether the

company has a positive net worth, whether it has enough cash and short-term

assets to cover its obligations, and whether the company is highly indebted

relative to its peers.

Cash Book:- The word “cash” represents the monetary

instruments (currency etc.) and the word “book” represents the record available

in written format. Thus, a cash book can be defined as the record of business

transactions in a particular period.

In other words, a cash

book records all transactions of cash receipts and disbursements (includes both

bank deposits and withdrawals). Cash book is divided into two parts namely,

cash payments and cash receipts.

Transactions which are

not recorded or are excluded in cash book are as follows −

v Transactions related to bank (payments made through checks

in receiving or paid).

v Non-cash transactions.

v Discount making or discount received.

v Cash book satisfies objectives of journal and a

ledger

Cash book as journal

v Just like a journal, it records transactions in

chronological order (as it happens).

v Follows the same procedure in posting transactions to ledger

from cash book.

v Maintains special cash books for cash transactions.

v Records cash transactions according to debit and credit.

Cash book as ledger

v Same format as ledger.

v Follows the same T format as ledger.

v Cash book balances are transferred to trial balance.

v Serve purpose of cash account.

Types:- The cash books

can be classified primarily into four different types that are:

1. Simple Cash Books -

These are also

known as Single Column Cash Books. They are used to record the cash

transactions and the cash receipts (cash that comes in) are entered on the left

side while the cash payments are recorded on the right side. As all cash

transactions are recorded in one book, there is no need for a cash ledger

account.

2. Two Column Cash Books -

In a two-column

cash book, there is an additional column provided for recording the specific

discount entries which allow the discount transactions to be recorded in the

same cash book along with the cash transactions. This cash book is usually

maintained by organizations where it is a general practice to give or receive

discounts.

3. Three Column Cash Books -

As the name

suggests, three-column cash books have three columns; one for cash, one for the

discount, and the additional bank columns. For most of the organizations that

are now dealing with banking instruments like cheques or bills of exchange

along with cash, a bank column in the cash book makes simplified accounting

entries.